Market Insights: All-Or-Nothing Days

Milestone Wealth Management Ltd. - Oct 21, 2022

Macroeconomic and Market Developments:

- North American markets were up significantly this week. In Canada, the S&P/TSX Composite Index advanced 2.92%. In the U.S., the Dow Jones Industrial Average rose 4.89% and the S&P 500 Index increased 4.74%.

- The Canadian dollar was positive this week, closing at 73.32 cents compared to 72.02 cents last Friday.

- Oil prices were mixed this week. U.S. West Texas crude closed at US$85.14 vs US$85.76, and the Western Canadian Select price closed at US$58.72 vs US$56.24 last Friday.

- The gold price finished higher this week, closing at US$1,655 vs US$1,643 last week.

- The political situation in the U.K. has been creating significant volatility in both equity and bond markets over the past few weeks, which saw incoming Prime Minister Liz Truss introduce tax cuts and additional stimulus into an already inflationary economy. This turmoil saw the new Chancellor of the Exchequer, Kwasi Kwarteng, resign his post last Friday. And ultimately, the culmination of the upheaval came with PM Truss resigning this week Thursday after just 44 days in the post, becoming the shortest serving Prime Minister in British history.

- Canada's biggest oilsands companies say they will spend $16.5 billion before 2030 on a massive proposed carbon capture and storage facility that is the centrepiece of their net-zero-by-2050 pledge. The Pathways Alliance is made up of member companies Canadian Natural Resources (CNQ), Cenovus Energy (CVE), ConocoPhillips Canada, Imperial Oil (IMO), MEG Energy (MEG), and Suncor Energy (SU).

- Continuing along that theme, U.K. energy company BP Plc has agreed to acquire biogas producer Archaea Energy (LFG), a Houston-based company which captures waste-gas emissions from landfills and farms, for US$4.1 billion including debt.

- Canadian inflation data was released this week, with the Consumer Price Index (CPI) up 6.9% from a year ago, higher than the expected 6.7% gain. While still high, the annual inflation rate has slowed for a third month, down from 7.0% in August, 7.6% in July and 8.1% in June.

- It was a busy week, with some high profile companies reporting earnings:

- Netflix (NFLX) reported upbeat results after the market closed on Tuesday with earnings of $3.10/share vs $2.13/share expected on revenue of $7.93 billion vs $7.837 billion expected. Also positive was the addition of 2.41 million subscribers vs an addition of 1.09 million subscribers estimated.

- Tesla (TSLA) reported mixed results after hours on Wednesday, with earnings of $1.05/share vs $0.99/share expected and revenue of $21.45 billion vs $21.96 billion expected.

- Snap Inc (SNAP), parent company of Snapchat, disappointed investors yet again after the market closed on Thursday. Earnings came in at $0.08/share, which was actually slightly better than the breakeven expected, although revenue was a bit light at $1.13 billion vs $1.14 billion expected. However, the big disappointment was in the 6.0% revenue growth which was lower than expected, sending the stock down 28.08% on Friday.

Weekly Diversion:

Do you ever wonder what your dog does when you’re not looking?

Charts of the Week:

In the last few weeks, we have tended to start off by saying “it was another wild one”. Not quite so much this week, where we have seen markets stabilizing to some degree in search of a major low and bouncing nicely off it’s 4-year moving average. The U.S. stock market advanced close to 5% this week and just over 6% from its intra-week low last week, while the Canadian stock market was up close to 3% this week and close to 5% from its last intra-week low. We have seen some strong support from institutional investors, who are buying at these levels from retail investors. This is often a sign of capitulation by retail investors, and usually a positive sign for forward-looking returns. Margin debt is off the record highs set last year, and the speed of deleveraging suggests excessive investor pessimism. The U.S. margin debt 15-month rate of change has recently entered an extreme oversold level not seen since 2001-2 and 2008-9. It has yet to turn back up, but when it does, equity markets have historically provided significantly above average gains up to 18 months later. Markets are also now heading into what is known as the seasonally strong period from the end of October to early May. In addition, there is the added potential tailwind of the third year of the U.S. presidential cycle (post-mid-term elections) which has historically been the best year out of the four.

Speaking to U.S. mid-term election years, this year has been tracking the typical pattern, albeit to a much greater degree of downside. But as we noted, equity markets have historically performed strongly leading up to the mid-terms and the 12-month period following.

Source: Nautilus Investment Research, FactSet

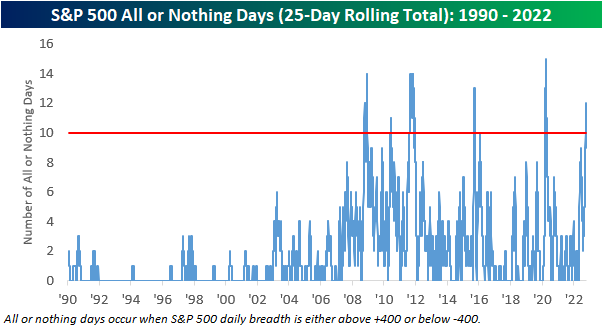

We will finish this week’s comment with a chart showing ‘all-or-nothing’ days for the S&P 500. An ‘all-or-nothing’ day is when the S&P 500’s advance/decline reading is less than -400 or greater than +400. In other words, more than 400 out of the 500 stocks are either all down or up on the day. On Monday, the number of these days on a 25-day (5-week) rolling total hit a level only seen a handful of times going all the way back to 1990. It hit a level of 12 days - which is just three days shy of the record set very close to the COVID crash low. In all, this is only the 6th time where this level has hit 10 or more days. In addition, the second chart shows these periods – indicated by red dots - on a chart of the S&P 500. As one can see, these periods have occurred at or near major long-term lows. The accompanying table below summarizes the forward-looking returns after these instances. Elevated numbers of ‘all-or-nothing’ days have historically coincided with weak and uncertain market environments like today. However, in the case of this signal which has occurred five prior times since 1990, that uncertainly led to opportunity, with historical forward-looking returns being on average 10.6% over the next six months and 24% over the next year - more than double the average for all other periods.

Source: Bespoke Investment Group

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group, @SentimenTrader, FactSet, Nautilus Investment Research